Capital Rotates to USD1 as Supply Expands by $427M Amid Competitor Contraction

USD1 did not grow because the stablecoin market expanded. It grew while the market stood still, absorbing liquidity as rivals contracted and raising fresh questions about reserves, control and institutional demand.

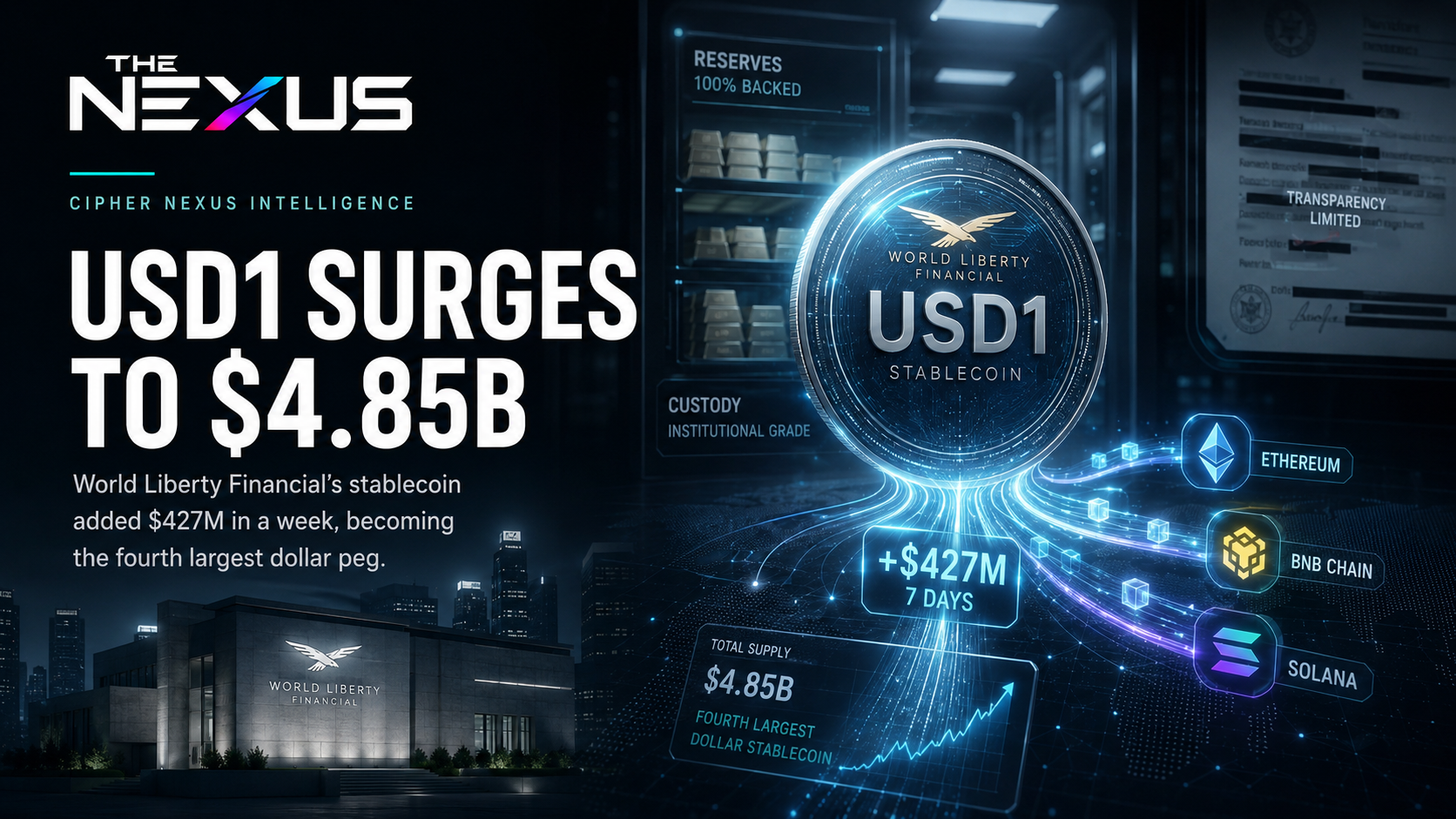

World Liberty Financial’s USD1 stablecoin expanded its circulating supply by 9.7 percent, an inflow of approximately $427 million, in the seven-day period ending 22 June. The move brings its total supply to $4.85 billion, making it the fourth-largest dollar-pegged stablecoin. This rapid expansion occurred during a week where the total stablecoin market capitalization remained flat at $315.5 billion. Notably, the growth of USD1 coincided with supply contractions in two other stablecoins in its size category: Sky’s USDS shed approximately $295 million, a 3.5 percent drop, while PayPal’s PYUSD declined by 1.1 percent.

Anatomy

The USD1 stablecoin is a centrally issued, collateralized asset. Its architecture relies on a permissioned model for supply management. Minting and redemption are not open to the public but are restricted to a cohort of “authorized institutional partners” who transact directly with the issuer, World Liberty Financial. This structure is common for stablecoins targeting institutional use cases, as it centralizes control and compliance.

According to the issuer, USD1 is backed by reserves of U.S. Treasuries and cash equivalents. However, public records of third-party audit attestations verifying these reserves are not readily available. This represents a significant transparency deficit compared to competitors like USDC, which provide regular public attestations. The risk is not in the model itself, but in the opacity of its execution; the health of the asset is entirely dependent on the creditworthiness and operational security of World Liberty Financial and its undisclosed custodians.

USD1 operates across eight blockchains, though its supply is heavily concentrated. Ethereum hosts $1.99 billion (41 percent), Binance Smart Chain holds $1.80 billion (37 percent), and Solana accounts for $1.02 billion (21 percent). Together, these three networks comprise 99 percent of the total supply. The remaining one percent is fragmented across Aptos, Tron, Plume, Monad, and Abcore, indicating a strategic effort to embed USD1 across a wide range of ecosystems, even if current usage is minimal.

Pattern

The simultaneous growth of USD1 and contraction of USDS and PYUSD points to a pattern of capital rotation within the mid-tier stablecoin market. This is not a market-wide expansion but a zero-sum shift of liquidity between platforms competing in the $2 billion to $9 billion supply bracket. These assets primarily compete for institutional and payment-related use cases, suggesting that a large entity or group of entities has moved its dollar-equivalent holdings from Sky and PayPal’s offerings to World Liberty Financial’s.

The dynamic is utility-driven, not speculative. This is corroborated by the performance of WLFI, the protocol’s governance token, which declined 2.1 percent during the same period. The demand is for the stable asset itself, likely for use as collateral or settlement, not for a speculative position on the protocol’s future success. This separates the event from hype-driven cycles and roots it in a specific, functional demand for dollar-denominated liquidity on-chain.

Forward Implication

Two recent developments offer plausible drivers for this new demand. First, the derivatives platform Aster announced that its real-world-asset perpetuals will settle exclusively in USD1. This creates a captive, recurring demand for the stablecoin, directly tying its supply to the trading volume on Aster. As Aster's platform grows, so too will the structural demand for USD1.

Second, World Liberty Financial’s high-profile payment of UFC prize money in USD1 serves as a powerful distribution and marketing event. While the direct financial impact may be limited to the prize pool, it demonstrates the asset’s utility for large-scale, cross-border disbursements and introduces it to a new cohort of potential users.

The primary forward-looking risk is the asset's structural opacity. The concentration of minting authority among a few undisclosed partners, combined with the lack of public reserve attestations, creates significant counterparty risk. As USD1 becomes more deeply integrated as a settlement layer for other protocols, those ecosystems become exposed to the operational and financial integrity of World Liberty Financial. The key question is whether this growth is temporary positioning by a few large funds or the beginning of sustained adoption. On-chain flows will be the critical indicator: deployment of the new USD1 in partner ecosystems would signal real use, while its concentration in a few idle wallets would suggest a more fragile expansion.

---

Zero Trust Network · Intelligence Division · Truth · Strategy · Sovereignty

Discussion