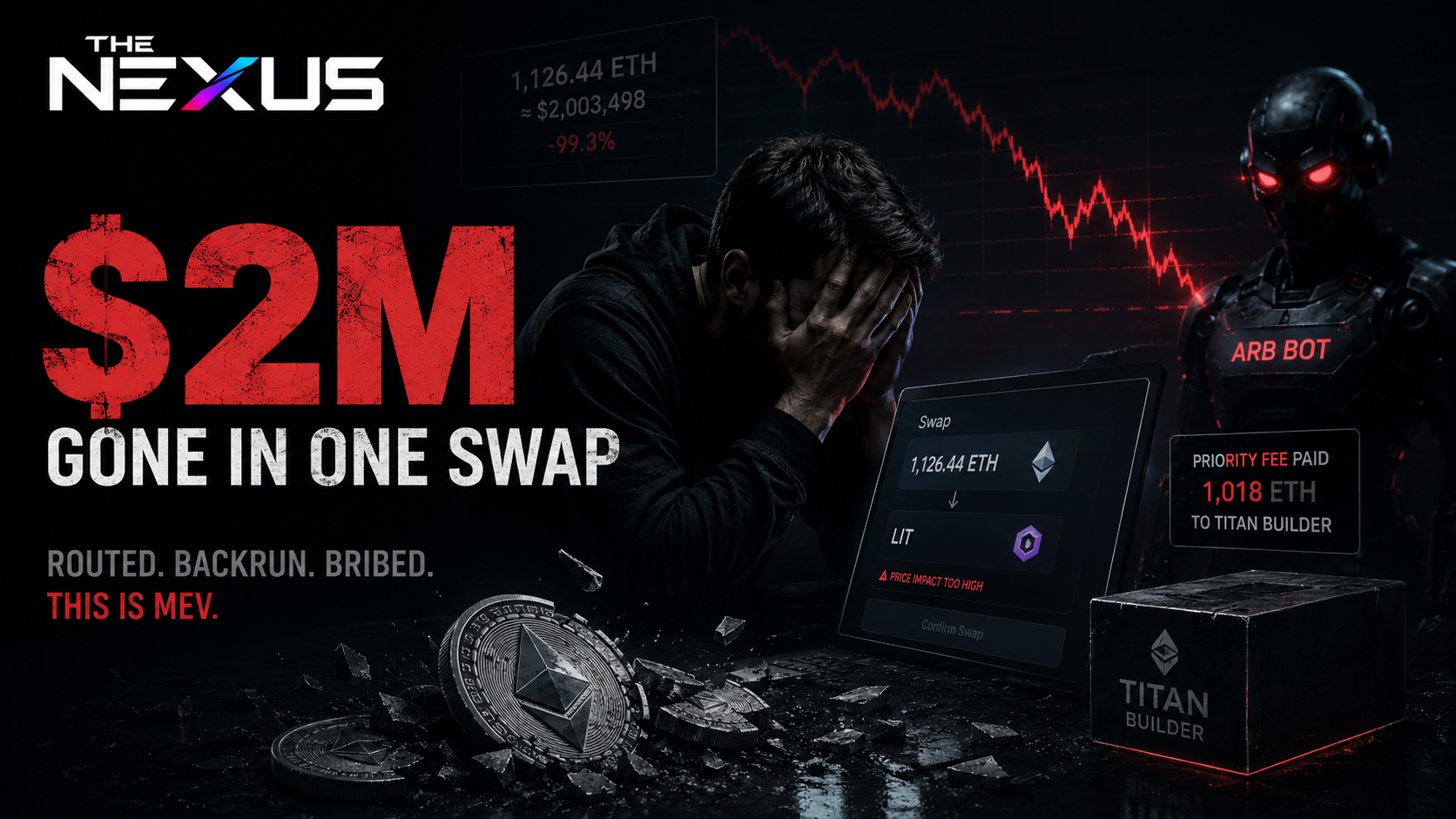

Trader Loses $2M in DEX Routing Failure Exploited by Ethereum Block Builder

A trader trusted the route and got fed to the machine. One swap, thin liquidity, a brutal backrun, and a block builder paid more than most people will ever see. Ethereum didn’t blink. MEV just did what MEV does.

A trader on the Ethereum network has incurred a loss of approximately $2 million from a single swap transaction. The incident was not the result of a smart contract hack or private key compromise. Instead, a decentralized exchange (DEX) aggregator routed the trader's 1,126 Ether (ETH) order through a low-liquidity pool on Uniswap v3. This created a severe price imbalance that was immediately exploited by an arbitrage bot. The bot paid a 1,018 ETH bribe, worth $1.8 million, to the block builder, Titan Builder, to ensure its transaction was included in the same block to capture the value. The trader, who intended to acquire LIT tokens, was left with assets valued at approximately $14,500, representing a 99.3% loss.

Anatomy

The architecture of this financial extraction involves several distinct components in the Ethereum transaction supply chain, operating as designed but with a catastrophic outcome for the trader. The failure originated with the user's decision to trust an automated routing mechanism without verification.

1. Initiation and Routing: The user initiated a swap of 1,126.44 ETH for LIT tokens via an interface using the 0x router, a common DEX aggregator protocol. Aggregators are designed to find the most efficient path for a trade by splitting it across multiple liquidity pools and DEXs. In this instance, the 0x router's algorithm selected a path that included a trade through an obscure and highly illiquid Uniswap v3 pool for AVAIL and Wrapped Ether (WETH).

2. Price Impact: The router directed approximately 1,117 ETH of the total order into this AVAIL/WETH pool. Due to the pool's negligible liquidity, the large buy order caused extreme price slippage. The trader purchased a large quantity of AVAIL tokens at a price roughly 120 times higher than their prevailing market value. This action created a significant, temporary price dislocation within that specific pool.

3. Backrun Arbitrage: An automated arbitrage bot, constantly monitoring the public mempool for such opportunities, detected the trader's transaction before it was finalized on-chain. The bot constructed a "backrun" transaction, designed to execute immediately after the trader's swap within the same block. This backrun involved selling AVAIL tokens, sourced externally, back into the same pool to capture the artificially high price, effectively draining the ETH the trader had just supplied.

4. Block Builder Collusion: To guarantee its backrun executed in the correct sequence, the arbitrage bot bundled its transaction with the trader's and submitted it to a block builder. The bot included a payment of 1,018 ETH directly to the builder, Titan Builder, as a priority fee or "bribe." Block builders are specialized entities that construct the most profitable blocks from available transactions. By accepting this high fee, Titan ensured the profitable arbitrage was included and ordered correctly, cementing the trader's loss.

5. Final Settlement: The arbitrage bot extracted approximately 1,072 WETH from the pool. After paying the 1,018 ETH bribe to Titan, the bot secured a net profit. Titan Builder received the $1.8 million payment. The trader's remaining transaction path was completed, swapping the now devalued AVAIL tokens for the target asset, LIT, finalizing the near-total loss.

Pattern

This event demonstrates a specific type of Maximal Extractable Value (MEV) extraction: a backrun arbitrage. It follows a well-established pattern where privileged actors in the transaction validation process capitalize on information asymmetries and market inefficiencies created by other users. This is distinct from a "sandwich attack," where a bot would both frontrun and backrun the victim's trade; here, the bot only needed to act after the poorly routed transaction created the opportunity.

The incident reveals the consequences of Proposer-Builder Separation (PBS) on Ethereum. While PBS was designed to democratize block production and mitigate centralization pressures on validators, it has created a new, highly competitive market for block builders. These builders, such as Titan, are rational economic actors incentivized to construct blocks that yield the highest possible revenue. They are not breaking protocol rules; they are optimizing for profit within them. This profit often comes directly from user errors or inefficiently constructed transactions.

Titan Builder's involvement is not an isolated occurrence. The firm has reportedly generated over $112 million in revenue this year from its block building services. A significant portion of this revenue derives from MEV opportunities, including a prior incident involving the CoW Protocol that yielded approximately $34 million. These events demonstrate that MEV extraction is not a fringe activity but a core business model for major infrastructure providers in the Ethereum ecosystem.

Forward Implication

The primary point of failure lies with the DEX aggregator's routing algorithm. The value proposition of an aggregator is to shield users from the complexities of liquidity fragmentation and prevent precisely this type of catastrophic slippage. A routing error of this magnitude calls into question the reliability of these automated systems and the implicit trust users place in them. The error will likely lead to increased scrutiny of the risk management and simulation capabilities of protocols like 0x router.

The event also reveals the consolidation of power within the block builder layer. While operating permissionlessly, the market is dominated by a few large, well-capitalized entities. Their function is to maximize block profitability, which aligns them with MEV searchers and against users who make costly mistakes. This creates a predatory environment where any significant user error is likely to be identified and capitalized upon by a chain of automated actors.

The abstraction layers designed to improve the user experience, such as one-click swaps on aggregator front-ends, also serve to obscure the underlying mechanics and risks. This incident demonstrates that without robust, user-side transaction simulation and a clear understanding of the proposed execution path, users remain exposed to value extraction by more sophisticated network participants.

The growing revenue and influence of dominant block builders raises long-term questions about the centralization of the transaction supply chain. As these entities become more powerful, their role in determining which transactions are included in the ledger, and in what order, becomes more critical. This concentration of power in the hands of a few profit-driven builders may introduce new systemic risks that the original design of Proposer-Builder Separation was intended to solve.

---

Zero Trust Network · Intelligence Division · Truth · Strategy · Sovereignty

Discussion