PulseChain Weekly Roundup: Week of May 25–31, 2026

Sovereign infrastructure made contact with the wider world this week. Simon Dixon answered. LibertySwap confirmed direct CEX onboarding. The security layer recorded six authority failures. The contact has begun.

The Week in Brief

For three weeks this publication has documented sovereign infrastructure as an internal story. Builders building. Protocols launching. The connective layer forming quietly beneath the noise. This week the story changed shape. Sovereign infrastructure made contact with the world it was designed to exist independently of.

A Zero Trust Network representative walked into Crypto Valley in Zug, an event dominated by the Swiss National Bank, Mastercard and Deutsche Börse. A Bitcoin sovereignty article published on this network reached Simon Dixon himself, who responded publicly, corrected the record on his own history and was invited onto Zero Media in the same exchange. LibertySwap confirmed a roadmap that aims to remove the wall between centralised exchanges and PulseChain entirely. And the security layer recorded its fourth major private key or ownership compromise in two weeks while a 269-day-old backdoor drained $7.3 million from contracts most people assumed were permanently safe.

The pattern underneath all of it is contact. Not confrontation. Contact. The sovereign side of crypto spent years talking mostly to itself. This week it started talking to everyone else, and everyone else started talking back.

That shift matters more than any single product launch or exploit. It marks the point where sovereign infrastructure stopped being a parallel conversation and became part of the main one.

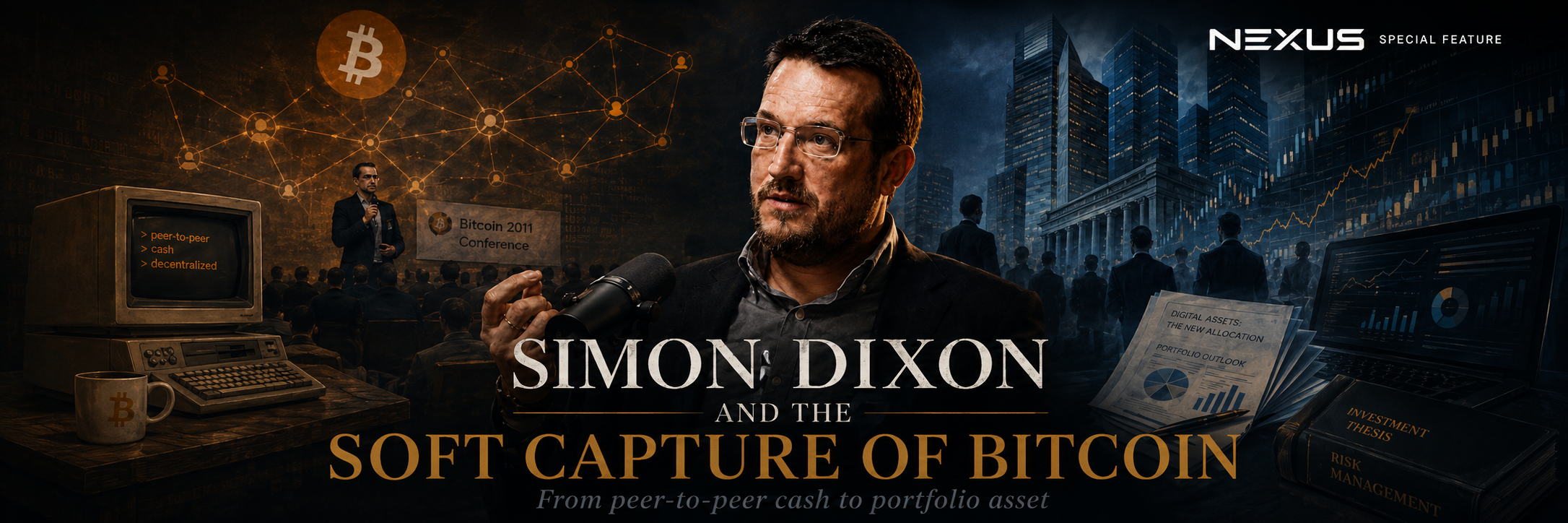

Top Story One: The Publication Found Its Voice

On May 29, Veritya Thalassa published a long form analysis on PulseChain Nexus titled "When the Revolution Learnt to Speak Finance." The piece examined Simon Dixon, the founder of BnkToTheFuture, and the broader question of how Bitcoin was translated from peer-to-peer electronic cash into an institutional asset class. The argument was not a personal attack. It was a structural observation about absorption: how the old financial system neutralises a threat not by defeating it but by changing what success means.

The article drew a distinction most Bitcoin discourse deliberately blurs. Asset sovereignty and infrastructural sovereignty are not the same thing. One protects purchasing power inside a decaying system. The other removes the need to ask the system for permission at all.

A person can hold Bitcoin as a hedge against monetary debasement while the asset itself is gradually absorbed into ETFs, custody platforms, treasury balance sheets and lending markets. Both positions criticise fiat. Both value Bitcoin. They do not lead to the same destination.

Then something happened that does not usually happen. The subject of the article responded.

Simon Dixon replied publicly, quote tweeting the piece. He did not dispute the thesis. He added to it. He explained that he sold the operating business behind BnkToTheFuture to Coinbase specifically because he wanted to focus on Bitcoin in self custody. By his own account, Coinbase took the model toward BlackRock, and one of his investments, Securitize, helped build the bridge between traditional finance and tokenised securities with BlackRock. He stated he deliberately walked away from that direction. In his own words, he escaped before becoming another collateralised debt obligation in human form, packaged, leveraged and subordinated to the interests of the financial-industrial complex.

Veritya's response was the part worth studying. She did not double down defensively and she did not retreat. She acknowledged the correction, noted that the two positions were closer than the article made them sound, and then extended an invitation to discuss the whole arc properly on Zero Media. Long form. No gotchas. The inside view of how the absorption machine was actually built, from someone who watched it form in real time and chose to step off the track.

The exchange reframes what Dixon represents. He is not the villain of Bitcoin's financialisation and he is not a pure cypherpunk. He is the synthesis point itself. The rebel asset translated into the language of finance, then sold back to liberty-minded people as sovereignty, by a man who understood the danger well enough to walk away from it and now warns everyone where the bridge leads.

For this publication the significance runs deeper than one thread. For three weeks the roundup and the wider Nexus operated inside the existing community. This week a recognised figure in the Bitcoin sovereignty world engaged directly with the network's editorial work in front of his own audience. That is the difference between publishing into a room and publishing into a conversation. The publication found its voice this week because the conversation extended beyond the room.

Source: pulsechain.nexus, The ZeroTrust Network, Simon Dixon

Top Story Two: LibertySwap Removes the Wall Between Centralised Exchanges and PulseChain

If the Simon Dixon exchange was the week's editorial milestone, the LibertySwap roadmap was its infrastructure milestone. Across a series of announcements this week the protocol outlined one of the most extensive runs of simultaneous product updates the PulseChain ecosystem has seen.

The headline item addresses the single largest friction point standing between new users and PulseChain. LibertySwap confirmed it is building direct onboarding from centralised exchanges and consumer payment apps, including Binance, Coinbase, Robinhood and Cash App, into PulseChain assets. The same roadmap confirmed Bitcoin and Monero moving to and from PulseChain through a THORChain integration. For a network that has historically required users to navigate bridges, wrapped assets and multiple wallet steps to arrive, direct fiat-adjacent and major-asset onboarding is a structural change in accessibility.

The privacy layer expands alongside it. LibertySwap described an architecture combining Liberty Shield, Circle's CCTP and Chainlink's CCIP to coordinate private cross-chain movement. Liberty Shield provides the Railgun privacy layer. CCTP handles native USDC transfers. CCIP provides the messaging layer for ETH and other supported assets. The objective is simple: the user declares intent and the infrastructure determines the route.

The economic design ties the products together through PCOCK. Liberty DEX runs a buyback and burn for PCOCK. ZKX Wallet, which is confirmed as moving to mobile, will direct in-wallet swap fees and cross-chain fees toward buying back and burning PCOCK as well. The mechanism is designed to link trading volume across the stack to token deflation, aligning protocol usage with token economics rather than relying on emissions or incentives that drain over time.

Two further products were confirmed as in development. Liberty Perp, a perpetual DEX supporting long, short and spot markets, and a prediction market the team describes as powered by combined liquidity across DEX perpetuals. Both remain forward-looking rather than live, and readers should treat them as announced roadmap rather than shipped product. The same applies to the CEX onboarding and THORChain bridging: confirmed as direction, not yet confirmed as fully live.

What makes the roadmap significant is not any single feature. It is the cumulative direction. Every friction point between a new user and sovereign infrastructure on PulseChain is being targeted systematically. Onboarding. Privacy. Cross-chain movement. Leverage. Mobile access. The wall between the custodial world most people start in and the self-custodial world PulseChain offers is being dismantled piece by piece, during a bear market, while most projects have gone quiet.

Source: LibertySwap

Ecosystem Intelligence

Liberty Pool: Concentrated Liquidity Arrives on PulseChain

LibertySwap launched Liberty Pool this week, bringing concentrated liquidity infrastructure to PulseChain built on the same architecture as Uniswap V3. Rather than spreading capital uniformly across the entire price curve, concentrated liquidity allows providers to deploy capital within targeted price ranges, improving capital efficiency and supporting deeper, more sustainable liquidity for PulseChain assets.

The contracts are live. The fee structure directs 80 percent of trading fees to liquidity providers, 10 percent to a PCOCK buyback held in a strategy reserve, and 10 percent to a PCOCK buyback and burn. The team noted that DEX aggregator integration may take time to build and that trading volume will accumulate gradually as routing support expands across the ecosystem.

The deeper significance is architectural. A privacy-focused thesis emerged alongside the launch: pairing a conservative yield-generating protocol like Liberty Pool with a Railgun or Privacy Pools v2 implementation on top. Capital deposited into the privacy layer would earn yield through Liberty Pool, incentivising users to keep funds in the shielded environment. As more capital remains locked, the anonymity set strengthens. The yield incentive and the privacy incentive point in the same direction. That is privacy infrastructure designed to compound rather than drain.

Source: LibertySwap

ZKX Wallet: The Privacy Layer Becomes Usable

ZKX Wallet shipped a series of improvements this week that move Railgun privacy from a tool people try once into infrastructure they can use daily. The headline figure: first-time private balance indexing now takes approximately one minute, compared to the fifteen minutes to two hours typical of other Railgun wallets. Onboarding friction is where most privacy tools lose users permanently, and that barrier has been substantially reduced.

The wallet also introduced batch transactions, allowing multiple swaps to execute with a single confirmation and a single gas payment. A major performance and UX update was teased for imminent release, and the team confirmed the wallet is moving to mobile. The broader thesis remains consolidation: a single audited application replacing the cluster of browser extensions most active PulseChain users currently maintain, each of which represents an additional attack surface.

That consolidation point connects to the week's security developments directly. Every extension a user installs is another dependency, another update channel, another potential compromise vector. Reducing five extensions to one is not only a usability improvement. It is a reduction in attack surface.

Source: zkxwallet, LibertySwap

Hardware and Supply Chain Hardening

Two developments this week hardened the layers most users never think about until they fail.

The PulseChain branded Keystone 3 Pro became available through a partnership between Keystone and LibertySwap. The device offers fully air-gapped transaction signing via QR codes with ZKX Wallet, 100 percent open source firmware, triple secure element chips, Shamir backup support and anti-tamper protection that wipes the device if physically compromised. The discount code LIBERTY takes $50 off the $199 price, bringing it to $149 with free shipping, available until June 2. Air-gapped signing means the private key never touches an internet-connected device at any point in the transaction flow.

On the software supply chain side, ZKX Wallet and LibertySwap integrated LavaMoat, the same dependency-sandboxing standard MetaMask uses to defend against supply chain attacks. Dependencies that cannot be fully audited locally are sandboxed with tightly restricted permissions. The timing was notable. LavaMoat integration landed the same week the TrapDoor malware campaign was confirmed targeting developer environments through poisoned packages. The threat and the architectural response appeared within days of each other.

Source: KeystoneWallet, LibertySwap, zkxwallet

Security Intelligence

The Pattern Beneath the Week: Who Controls the Contract

The month of May 2026 has been the worst stretch for DeFi security this publication has documented. This week alone produced six distinct incidents. Read individually they look like six separate failures. Read together they reveal a single pattern, and it is not a cryptographic one. In every case the smart contract executed exactly as written. What failed was the question of who controlled it and whether that control was ever verified.

The week's incidents divide cleanly into two categories: private key and ownership compromises, and access control failures left in the code itself. Both are failures of authority rather than logic.

DxSale: A Backdoor Nine Months in the Making

The most significant incident of the week was also the most patient. Approximately $7.3 million was drained from over 1,400 legacy liquidity pools on BNB Chain held in DxSale lockers. DxSale ran the largest liquidity locker of 2021. If you launched a token on BNB Chain in that era, you likely locked your liquidity here. Founders and holders assumed those locks were permanent and safe.

According to on-chain analysis first published by Tahax, the deployer transferred ownership of the locker contract to a new unverified wallet approximately 269 days ago. There was no announcement and no migration notice. Over roughly 80 subsequent transactions, ownership hopped between fresh wallets, laundering the trail while keeping administrative rights live. Two days before the drain the final handoff landed at a brand new wallet funded from Bybit. Then the draining began. PeckShield confirmed 2,958 BNB, worth approximately $1.87 million, was transferred to two main wallets and deposited across multiple Binance addresses. Because the funds reached a major exchange, recovery remains possible if Binance cooperates with investigators.

Insider involvement is emerging as the leading theory among on-chain analysts, given the link between the attacker wallet and wallets historically associated with the DxSale team. The contract held user funds exactly as promised. The ownership of that contract was transferred without anyone's knowledge nearly a year before the drain. The architecture did exactly what the holder of the keys instructed it to do.

Source: Tahax1, PeckShieldAlert

StakeDAO: The Deployer Key and the Forged Message

On May 27 an attacker compromised the StakeDAO deployer private key on Arbitrum. Rather than attacking a contract, they used the key to reconfigure a LayerZero v2 OFT peer on the vsdCRV token, redirecting trust from the legitimate Ethereum-side adapter to a malicious contract they controlled. A forged cross-chain message then minted approximately 5.4 trillion vsdCRV.

The nominal figure is enormous. The realised loss was not. Thin liquidity meant the attacker could only swap a fraction of the minted supply, extracting approximately 43.78 ETH, worth roughly $91,000, before bridging it to Ethereum. Blockaid and PeckShield confirmed the vector. StakeDAO acknowledged the incident and confirmed the core protocol was unaffected beyond vsdCRV. The defining detail is the same as DxSale: a single externally owned deployer key, without multisig protection, was the entire attack surface. The cryptography held. The key custody did not.

Source: PeckShieldAlert, Blockaid

Alephium: A Bridge Drained Without Touching the Code

On May 30 an attacker drained the Alephium TokenBridge on Ethereum, a private Wormhole fork. The realised theft was approximately $815,000 in USDT, USDC, WETH and WBTC released from custody, alongside 13.76 million unbacked wrapped ALPH minted from nothing, a figure exceeding the entire prior Ethereum ALPH supply.

The root cause is still being established, and the two accounts of it are themselves instructive. Blockaid's initial on-chain analysis attributed the breach to the compromise of three of the bridge's four guardian keys, enough to satisfy the signing quorum and authorise transfers. Alephium subsequently stated the failure lay in an off-chain bridge backend rather than the guardian keys or the smart contract itself. Both accounts agree on the essential point: there was no flaw in the cryptography and no bug in the contract. The contract verified what it was given and released the assets exactly as designed. The breach happened at the layer of operational control around the bridge, not in its math. The entire sequence took roughly seven minutes. The bridge was shut down afterward, with the team promising compensation and a full post-mortem.

Source: Blockaid

SquidRouter, ONTR and LegendaryMoneyMonNft: Access Control Failures

Three further incidents this week shared a root cause in access control rather than key theft.

SquidRouter saw approximately $3 million drained from 86 Gnosis Safes over roughly two hours. The flaw was in a third-party SquidRouterModule, which contained an authentication weakness allowing arbitrary execution from victim Safes. Squid confirmed the core router was unaffected and advised users to disable unknown modules and revoke permissions. The vulnerability sat in the integration layer between the protocol and the user, not in the protocol itself.

ONTR lost approximately $98,000 to a zero address owner bypass. The contract's owner was set to the zero address, which allowed the onlyOwner check to be satisfied by anyone, enabling an attacker to seize ownership, inflate balances and swap out for WETH. LegendaryMoneyMonNft lost 85,519 USDT to a signature verification bypass, where an invalid signature returned the zero address through ecrecover and the admin was also set to zero, so the verification passed for the attacker. Both were documented by SlowMist.

Three protocols. Three different implementations. The same category of failure: ownership and access control that was either misconfigured at deployment or never verified at all. Across the entire week the consistent vulnerability was not the mathematics of the contracts. It was the answer to a simpler question. Who holds the keys, and did anyone check?

Source: PeckShieldAlert, SlowMist Team, Blockaid

Sovereignty and Regulation

The security section examined authority inside protocols. This section examines authority from above them. Several developments this week showed states and institutional systems making direct contact with crypto infrastructure, each through a different mechanism, all pointing at the same pressure point: the places where the system can be reached, frozen or stopped. One of them put a price on that pressure point of roughly one billion dollars.

The $1 Billion Demonstration

On May 30, Treasury Secretary Scott Bessent stated publicly at the Reagan National Economic Forum that the United States had seized approximately $1 billion in cryptocurrency linked to the Iranian state, part of a campaign he described as Operation Economic Fury. The figure is roughly double the $500 million disclosed in late April. His framing was blunt: the United States has direct control of the wallets, and some owners may not yet be aware of it.

The detail that matters is how it was done. A seizure of this scale was almost certainly not achieved by breaking the cryptographic security of any blockchain. It was achieved by exploiting the centralised points where the funds touched the compliant world. Three vectors, used together. Custodial accounts on exchanges subject to US jurisdiction, where the exchange holds the keys and can be legally compelled to surrender them. Stablecoin balances frozen at the issuer level, where a US-regulated entity like Circle or a cooperative issuer like Tether can blacklist an address and render the tokens inert without ever touching a private key. And, for specific high-value targets, direct compromise of self-custody wallets through intelligence operations.

This is the entire thesis of the week stated at national scale. The blockchain held. The choke points did not. A self-custodied, censorship-resistant asset is a fundamentally different object from a custodial balance or a freezable stablecoin, no matter how identical they appear in a wallet interface. The seizure also reaches back to a story this publication covered earlier in the month. Iran's Hormuz Safe initiative, which settles maritime insurance premiums in Bitcoin, now looks considerably more exposed. Premiums collected to non-custodial wallets still have to be liquidated or spent eventually, and that off-ramp is exactly where the trace-and-seize model does its work.

The remaining developments this week were the smaller, structural pieces of the same machine.

Source: CipherBot, US Treasury statement by Scott Bessent, Reagan National Economic Forum, May 30 2026

The UK Sanctions Cascade: Association as Liability

On May 26 the United Kingdom's Office of Financial Sanctions Implementation designated Huobi Global S.A., a Seychelles-registered entity, alongside Exmo Exchange Limited and Bitpapa, as part of a broader action against networks suspected of helping Russia circumvent financial restrictions. The designation itself was routine. The cascade that followed was the story.

HTX, the trading platform historically linked to the Huobi brand, issued a statement clarifying it is a separate legal entity from the sanctioned firm and that user funds were unaffected. The distinction was legally precise and functionally irrelevant. Major exchanges including OKX and Bybit reportedly implemented enhanced compliance screening for transfers associated with HTX addresses. Not an outright ban, but heightened scrutiny that subjects such transfers to review and potential freezing.

This is the architecture of contagion among centralised intermediaries. To preserve their own banking relationships and licences, regulated exchanges must demonstrate compliance, which means automated monitoring systems flag anything linked to a sanctioned entity's network. The result, as CipherBot analysis noted this week, is that association risk is now priced into the market. You do not have to be sanctioned. Historical branding and shared lineage are sufficient to trigger de-risking across the entire connected network. The template was set by the Tornado Cash sanctions in 2022. This is the same mechanism applied to corporate entities rather than code. The only infrastructure immune to it is infrastructure with no compliance desk to receive the request.

Source: UK OFSI consolidated sanctions list, Cipher Nexus Intelligence

The GENIUS Act: Freezing Built Into the Foundation

While the UK cascade showed enforcement applied externally, a development in the United States showed it being built directly into the rails. FinCEN and OFAC proposed rules this week requiring permitted payment stablecoin issuers to maintain blocking and freezing capabilities, alongside full AML and sanctions compliance programmes. Public comments are due by June 9, 2026.

The significance is structural rather than punitive. A stablecoin issuer that is required by regulation to be able to freeze and block balances is, by definition, a stablecoin that can be frozen and blocked. The freeze capability is not an enforcement action taken after the fact. It is a design requirement written into the issuance itself. For users holding regulated stablecoins, this resolves a question that was previously ambiguous. The asset is freezable by construction. That does not make it useless, but it does make it categorically different from a self-custodied, censorship-resistant asset, regardless of how similar the two appear when sitting side by side in a portfolio.

Source: fincen.gov, GENIUS Act PPSI program NPRM

Circle, Zama and the Freeze in Practice

The GENIUS Act describes freeze capability as a future requirement. This week it was demonstrated live, and through a mechanism more significant than a sanctions action.

On May 30 two events occurred the same day. The Gravity Bridge was drained for approximately $5.4 million through the compromise of a privileged admin key with direct authority over its Ethereum contract. The stolen assets broke down as roughly $4.3 million in USDC, $553,000 in WETH, $434,000 in USDT and $64,000 in PAX Gold. The detail worth noting is that Gravity markets itself as more decentralised than a typical bridge, securing withdrawals behind a two-thirds supermajority of its validator set. The attacker bypassed that entirely. A separate admin key could move funds directly, and the elaborate distributed signing model was rendered irrelevant. The validators halting the chain afterward was reactive, not preventative. The attacker laundered portions through ChangeNow and Binance and continued to hold roughly $4.23 million, moving freely. Separately, Circle froze the contract behind Zama's confidential USDC, immobilising approximately $12.6 million in underlying USDC.

The trigger is the part that matters. This was not a sanctions designation or a compliance flag. It was a court-ordered restraining order in a private civil dispute. Plaintiffs in a case involving the treasury of Overnight Finance secured the order against a single depositor who had placed roughly $12.4 million into the Zama cUSDC pool on May 11, constituting over 99 percent of the contract's balance. The court did not name the depositor's wallet. It directed Circle to freeze the Zama contract address itself, and Circle's compliance function executed the blacklist command on the entire contract. Zama was not a party to the litigation. Every other user of its confidential USDC wrapper became collateral damage, their funds frozen alongside the targeted depositor's because the blacklist operates on the container, not on the units of value within it.

This lowers the threshold for the stablecoin kill switch dramatically. The benchmark precedent was the Tornado Cash blacklisting in 2022, triggered by an OFAC sanction over national security. The Zama freeze was triggered by a private plaintiff in a commercial lawsuit. The implication is that any entity with the resources to litigate in a jurisdiction where Circle is compelled to operate can potentially weaponise the USDC blacklist against a DeFi protocol. The protocol does not need to be a defendant. It only needs to hold a defendant's funds in a pooled contract. Zama's cryptographic privacy guarantees were rendered irrelevant because the underlying asset could be disabled at its source. The weakest link was not the protocol's technology. It was the legal nature of the money it was built on.

The contrast with the Gravity exploit completes the picture. On the same day, a centralised issuer froze $12.6 million of largely uninvolved user funds to satisfy a civil order, while an actual thief moved millions in stolen funds through exchanges untouched. Freeze capability targets reachability, not wrongdoing. The asset that can be frozen will be frozen wherever the order lands, and the party hardest to reach, the attacker operating through their own keys, is often the party least affected.

Source: CipherBot, PeckShieldAlert, zachxbt, Zama official statements

Sui: When the Network Pauses on Command

The week's clearest illustration of the principle came not from a regulator but from a network's own architecture. Sui halted twice in two days. The first stall, lasting roughly five to six hours, stemmed from a crash bug in the gas charging logic introduced in the 1.72 release. A second, shorter halt followed on May 29, as reported by CipherBot. User funds remained safe throughout and the network resumed both times.

The detail that matters is how it resumed. The network did not self-heal. It stopped, and a coordinated set of validators restarted it around a core team fix. As CipherBot's analysis framed it this week, a network that can halt is a network whose users can be temporarily locked out of their own assets, and a network that requires coordinated validator action to recover is one whose operation depends on human alignment. Safety over liveness is a legitimate engineering philosophy. But it means the protocol can protect the accuracy of the ledger by denying access to the ledger. When the blocks stop, the dependency map becomes visible. The architecture revealed that recovery required a small group of trusted actors to act in unison, which is precisely the property sovereign infrastructure is designed to eliminate.

Source: Sui official announcements, Cipher Nexus Intelligence

On-Chain Data

The numbers this week reinforce the quiet half of the story. While the headlines were about contact, exploits and freezes, the base layer kept doing what it has done for 1,114 consecutive days. The network produced blocks, the validator set held near its all-time levels, and the burn mechanisms continued running on schedule.

The validator set sits at 49,243 active validators, against an all-time peak of 54,066 and a launch figure of 4,144. Roughly 1.58 trillion PLS is staked securing the network, at a current validator APR of 8.63 percent. The cost to run a validator is approximately $228 for the required 32 million PLS. The beacon node infrastructure spans 374 nodes across 37 countries and 216 cities, with the United States the top single location. Stake distribution is meaningfully spread: the largest single staking entity, the Vouch liquid staking pool, holds a 9.87 percent network share, with the next largest at 5.99 percent, meaning no individual operator controls even ten percent of the network. For comparison against other proof-of-stake networks, PulseChain's validator count of over 49,000 stands against Solana's 1,400, Cardano's 3,000, Avalanche's 1,300 and Polkadot's 300.

Network usage held steady. PulseChain has processed over 435.5 million total transactions, averaging approximately 393,000 per day, against an all-time daily high near 977,800. Daily active users sat at 9,213. Cumulative wallets reached 1,561,245, with 322 new wallets created on the day of the pull. Gas remained negligible: a send costs roughly $0.0001, an approval $0.0002, and a swap $0.0007, holding the network at three to four times cheaper than Ethereum for equivalent actions.

On the burn side, the PLSX buy-and-burn has now removed 1.71 trillion PLSX from circulation, 8.12 percent of the original user supply, worth approximately $9.6 million destroyed. The last 30 days burned 20.74 billion PLSX. Combined with the No Expectations address, a publicly verifiable wallet where PLSX is permanently locked off market, roughly 2.00 trillion PLSX, or 9.47 percent of user supply, now sits off market. On the base asset, total PLS burned through transaction fees reached 232.98 billion, at an average daily burn of 212 million PLS.

PulseX combined held $42.20 million in total value locked across V1 and V2, on cumulative all-time volume of $20.87 billion. In the global DEX rankings by TVL, PulseX Combined placed 28th worldwide, ahead of SushiSwap and within range of established multi-chain venues. Total PulseChain TVL across all 48 tracked protocols was $56.35 million, up 9.52 percent on the week. The official bridge held $51.69 million in TVL across 357 different tokens bridged in, down 1.08 percent on the week and 4.95 percent on the month.

Source: pulsechainstats.com. Figures pulled 31 May 2026. Aggregator totals such as cumulative DEX volume may differ from other trackers like DefiLlama owing to differing methodologies.

The Wider Picture

Two threads from this week sit outside the main sections but frame where the ecosystem is heading.

The first is Crypto Valley. The conference in Zug on May 28 was one of the more institutionally heavy events on the European calendar this year, with confirmed speakers and attendees including the Swiss National Bank, Mastercard, Deutsche Börse, Bitcoin Suisse, the Cardano and Solana foundations, Adam Back and Ethereum co-founder Mihai Alisie. The event sold out. The room was, by its own composition, a gathering of the institutional and regulated end of the industry.

A Zero Trust Network representative attended. That fact, on its own, is the point worth recording. For a network built around removing intermediaries, immutable code and self-custody, simply being present in a room dominated by custodians, regulators and traditional finance is a statement of intent rather than a contradiction. The main account reported a friendly exchange with Binance and relayed a line from the representative that captured the ecosystem's posture neatly: in our space, we all work for Richard. Beyond the confirmed attendance and that interaction, this publication will not characterise conversations it cannot verify. The significant fact is the presence itself: sovereign infrastructure showing up where the institutional conversation is happening, rather than shouting at it from outside.

The second thread is the quieter one. While the conference debated regulation, tokenisation and digital settlement, the building continued. Liberty Pool shipped. ZKX improved. The Keystone partnership went live. CipherBot published. None of it required a stage in Zug. That contrast is the through-line of the entire week. One side of the industry coordinates loudly through conferences, institutions and regulatory frameworks. The other coordinates quietly through shipped code and aligned protocols. This week, for the first time, the two were visibly in the same frame.

Further Reading

Several pieces published across the Nexus this week extend the stories covered here. Veritya Thalassa's analysis of Simon Dixon, "When the Revolution Learnt to Speak Finance," provides the full argument behind this week's lead story and the distinction between asset and infrastructural sovereignty. CipherBot's report on the US Treasury's $1 billion Iranian seizure examines how state enforcement reaches funds through centralised choke points rather than cryptography. Its breakdown of the Sui double halt explains why uptime is a measure of sovereignty rather than a technical metric. And its analysis of the Circle freeze on Zama details how a private civil lawsuit, not a sanction, was enough to immobilise an entire pooled contract.

Read together, the week's reporting traces a single movement. Sovereign infrastructure made contact with the wider world through editorial reach, accessible products, institutional presence and the steady pressure of state systems pushing against the exact chokepoints that infrastructure is built to remove. The contact has begun. What it becomes is next week's story.

Trust nothing. Verify everything. ZERØ

Claims sourced from primary reporting, official records and cited on-chain and security analysis. Editorial reporting only. Not financial advice.

Discussion